A detailed breakdown on why Islamic mortgages are backdoor riba

Problems with Guidance Residential

Most of the Islamic mortgage companies operate similarly. So I will take the most common example in the United States — Guidance Residential.

Guidance says their home purchase is two contracts. The first one is Musharaka. The second one is Ijara. The first contract is the commitment to buy the house over 30 years. The second contract is the “rent agreement”. Together, they function as a diminishing co-ownership agreement. In practice, Guidance and the homebuyer form an LLC. Then the LLC purchases the house, with all of the transactions occurring at the closing table.

There are some clear problems with the transaction.

Guidance does not own the home, but is selling you a rent-to-own agreement. Our Prophet ﷺ forbade selling what we do not own. Throughout the entire process, Guidance never holds the title to the home.

Our Prophet ﷺ forbade selling what we do not possess. Yet, Guidance has you sign a “rent to own” agreement, before Guidance has closed on the house. In Islam, Guidance can not ask you to sign an acquisition agreement, until they have bought the house and taken possession of it. Guidance did neither. Abu Hurarira (R), Abdullah bin Abbas (R), and other Companions knew permitting these transactions would allow riba.

Guidance conditions one contract on another contract. Guidance admits that you can’t sign one without signing the other. Our Prophet ﷺ forbade combining contracts, and Abdullah bin Umar (R) forbade it as well. A type of “buyback sales” was called Bay’ al Inah’ transactions which were directly condemned by the Prophet ﷺ. In effect, Guidance is combining contracts to mimic riba. The Prophet ﷺ was aware of this deception.

If Guidance had owned the property before reselling, they would be required to pay fees and taxes twice. Guidance avoids double fees by not owning the property. There are several fees associated with purchasing a home, such as appraisal fees, home inspection fees, closing costs, property taxes, capital gains tax, and others.

Behind the scenes, as soon as you sign the contracts, a simultaneous transaction occurs. Guidance sells the agreement to Freddie Mac.

In Islam, you can make and sign contracts, but you can’t sell contracts to third parties. Selling contracts is a form of riba. In effect, it’s just a money exchange, not a sale of assets. Our Prophet ﷺ forbade money exchange with a delayed payment in the future.

When Guidance signs up 100 people, they don’t actually have $40 million to lend. They get the borrowers to sign the mortgages, and then sell them to Freddie Mac at a slight discount. And Freddie sits on the mortgage for 30 years, collecting principal and interest. This is well-known, and even the AMJA fatwa makes it clear that this transaction is impermissible.

When purchasing a house with a Guidance mortgage, payments go to Freddie Mac, as the contract was sold to them. It's puzzling how Guidance claims co-ownership when Freddie Mac receives payments.

Some Muslims will turn a blind eye, and pretend this part of the transaction is none of their business. However, they are part of the transaction. Is it halal to sell a sword to someone who you know will use it for murder? Similarly, it’s not a suitable excuse to turn a blind eye to Guidance selling their agreement to Freddie Mac.

It is worth noting that this practice is also called “derivatives trading”, which can take the form of the futures market, swaps, or options that are impermissible for the same reason.

The Prophet ﷺ forbade two sales in one sale. In the case of an invalid contract such as this arrangement, he said any difference in sale prices is considered riba. With the Guidance contract, the price of the house isn’t fixed. The final sale price of the contract is different if the home is paid off in 5 years, 15 years, 20 years, 30 years, and so on. The contract should have the price of the home pre-determined and fixed at the signing of the contract. This is also an example of gharar — significant uncertainty. Gharar transactions are forbidden by the Prophet ﷺ.

In true co-ownership, investment shares are treated as assets. With Guidance, the home is collateral. They put a lien on the house. In the event of foreclosure, short sale, or home loss of value, Guidance doesn't share losses. If the foreclosed house sells for $100,000, even if you own 20%, the foreclosed party doesn't get any of that 20%, until Guidance is paid off. The Prophet ﷺ forbade transactions in which losses are not equally shared.

Investments share costs. Guidance doesn’t share costs. It doesn’t pay property tax. It doesn’t pay insurance. It doesn’t pay Homeowner Association fees. It doesn’t pay for house maintenance. Guidance argues, “We don’t benefit from those services”, but it’s not true as Guidance does benefit. Regardless of Guidance semantics, expenses must be shared in an Islamic investment. Paying those things is hinged upon ownership, not whether anyone benefits from that service.

If it was truly rent, then the renter would be paying for the right to use the property. In this contract, rent is due even in default. The renter is obligated to pay regardless of whether the person has access to the property or not, such as in default. Guidance can not charge rent for a property it no longer owns. Additionally, if the agreement was a genuine lease, then the future tenant's rent would be used to offset unpaid rent.

Indeed, every legal entity considers it a loan. Guidance, Freddie Mac, loan services, IRS, courts. They aren’t listed as a co-owner on the title. They are even licensed as a mortgage lender. Even the quarterly reports of the publicly traded Islamic mortgage companies show it as a loan. Everyone treats it as a loan, except you — the borrower.

The home investment is not halal by AAOIFI criteria — the halal standard for investing in stocks. Most mortgage lenders fund the home purchase with riba loans, so it should not pass a AAOIFI financial screen. Guidance claims self-funding for home purchases, but admits it obtains external funding through an agreement with Freddie Mac. It’s worth noting that some of the same people on AAOIFI Shariah board were on the Guidance Shariah board, and they overlooked this issue. Ironically, some Muslims seek halal stocks, but their home wouldn't meet basic AAOIFI standards.

The rent and house are not sold to the customer at fair market value. The “halal” mortgage is just benchmarked to the interest rate of the central bank. The mortgage payments are unaffected if the house value goes down.

Commentary

This speaks to the brilliance of our Prophet ﷺ. He didn’t just forbid riba. He forbade all the loopholes as well, even if the Muslims who love riba wanted to get cute.

The “Islamic mortgage” contract is a replica of a European contract known as contractum trinius. This was used by money lenders in Europe to circumvent the Church laws against usury. Speaking of mortgage, “mortgage” literally means “death pledge” in it’s Latin-French roots. And the Muslim community is knee-deep in riba.

In the United States, Islamic mortgages are a multi-billion dollar industry. It’s worth noting that many of these corporations — UIF or Devon Bank — are not owned by Muslims. The business is so lucrative that Guidance sued UIF in 2014 for stealing “trade secrets”. They both view the Muslim community as a “trade secret” to be exploited. And it is clear from court records that they consider these loans as interest-bearing loans.

Today, Islamic banks are paying hundreds of thousands of dollars to Islamic scholars to label Islamic mortgages as permissible. Is it appropriate for Islamic mortgage companies to send “muftis” on sponsored vacations to Makkah? Virtually akin to how the Israel lobby operates. We can put our heads into the sand, and pretend this is not the case. Or confront the reality that this is a serious problem.

Sadly, the word “Sharia compliant” is as meaningless as “zakat eligible”. This is a form of false advertising. Adding fancy Arabic words does not make riba permissible. The term “Islamic financing” is problematic in itself as it implies that there is a profitable way to lend. Allah only allows loans for benevolent reasons. That's why loans are such a good deed. On the opposite end, any benefit from a loan is considered riba.

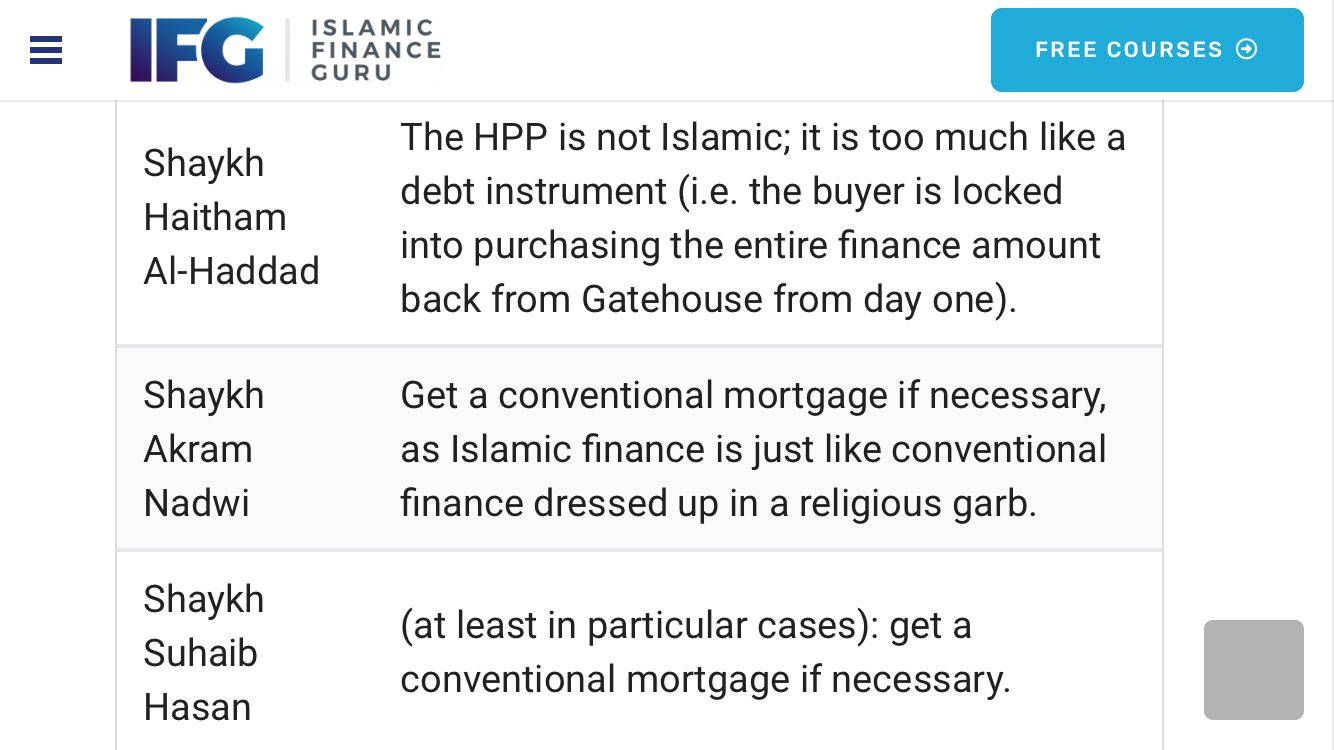

Do Islamic mortgages sound like mental gymnastics to charge interest? Does Guidance sound like a pawnbroker who holds the house as collateral until the borrower repays the loan with interest? Many Islamic scholars have already spoken out against Islamic mortgages.

My scholar said it’s halal, so it’s halal

“I always wonder what people mean by fatwa? And for that matter who is considered a scholar? Is a scholar the person who tells us what we want to hear? So the onus returns to us to verify that a ruling by anyone is legit. Is the ruling based on the Quran and Sunnah? Or just throwing out an opinion? Companions themselves would question each other about their sources.”

The words above.. they aren’t my words. But they deserve to be reiterated. The Quran warns that previous nations took the word of some of their scholars over Allah and His Messenger ﷺ. Although they didn’t literally worship their scholars, Allah describes their action as taking “lords besides Allah”. Just like all Quran stories, this is worth reflecting on. Surely, there is a valuable lesson in these verses.

They have taken their scholars and monks as lords besides Allah, and [also] the Messiah, the son of Mary. And they were not commanded except to worship one God; there is no deity except Him. Exalted is He above whatever they associate with Him.

Sabbath breakers

The proponents of Islamic mortgages are reminiscent of the Sabbath-breakers mentioned in the Quran. Allah forbade riba, so they invented a workaround.

Similarly, Allah forbade a group of people from fishing on the Sabbath. They were tested because fish would only come on Sabbath. So, this group set up fish traps before the Sabbath and collected the fish after the Sabbath. Allah punished them by transforming them into monkeys and pigs. A fitting punishment for those who clown with Allah’s commands.

A Prophetic warning to the Ummah

Indeed, our Prophet ﷺ predicted this moment.

Messenger of Allah ﷺ said,

Indeed, Allah does not take away knowledge by snatching it from the servants, but He takes away knowledge by taking away the scholars until, when no scholar remains, people will take ignorant leaders. They will be asked [for religious verdicts], and they will issue verdicts without knowledge. They will go astray and lead others astray.

Messenger of Allah ﷺ said,

Among the signs of the Hour are: wealth will become abundant and widespread, trade will increase, knowledge will become apparent, a man will make a sale and say 'No [I won't conclude the sale] until I consult the merchant of such-and-such family,' and in a great neighborhood a literate person will be sought but will not be found. And people will search in a populous area, they will look for a record-keeper but won't find anyone.

This is part of my series on Interest Free Zone: All of the Sahih hadith related to riba, A study of weak hadith on riba, Defining riba, A detailed breakdown on why Islamic mortgages are backdoor riba, Do credit card rewards programs have riba?, Madness on options riba

Related, I have a Riba and Ruin series: Economics is to keep you a dummy, What happened to SVB?, Ward of the State, First Republic: A tale of a fake bank & a fake auction, Hush, hush, a small bank goes poof

Related, I have a Selling Islam series: Salaried Shaykhs, Can paid Shaykhs make mistakes?

References

AMJA Resident Fatwa Committee. (2018). Resolution about Islamic home financing companies in the US. AMJA Online. https://www.amjaonline.org/amja-resident-fatwa-committee-resolution-about-islamic-home-financing-companies-in-the-us/

Durr, M. (2016, June 23). Ann Arbor bank ordered to pay $1.1 million for breaking trade secrets law. MLive.com. https://www.mlive.com/business/ann-arbor/2016/06/ann_arbor_bank_ordered_to_pay_2.html

El-Diwany, T. (2006, July 13). Banks subvert Islam's ban on usury. Financial Times. https://www.ft.com/content/3507f192-1296-11db-aecf-0000779e2340

Goldstein, J. (2016, May 14). Episode 701: A bank without interest. Planet Money. NPR. https://www.npr.org/transcripts/477956675

IslamQA (2013, December 1). Selling at the original price and making maintenance and insurance the responsibility of the customer in a diminishing share partnership. IslamQA.info. https://islamqa.info/en/answers/242216/selling-at-the-original-price-and-making-maintenance-and-insurance-the-responsibility-of-the-customer-in-a-diminishing-share-partnership

Muhammad bin Adam (n.d.). Permissibility of leasing one's property. IslamQA.org. https://islamqa.org/hanafi/daruliftaa/7893/permissibility-of-leasing-ones-property/

Qutub, H. (2012, May 8). Response to Muslim Matters Post on Halal Mortgages. MuslimMatters. https://muslimmatters.org/2012/05/08/response-to-muslim-matters-post-on-halal-mortgages/

Usman, O. (2012, March 26). Halal Mortgages: Misuse of Taqi Usmani Fatwa and Other Important Questions. MuslimMatters. https://muslimmatters.org/2012/03/26/halal-mortgages-misuse-of-taqi-usmani-fatwa-and-other-important-questions/

Qutub, H. (2012, May 8). Response to Muslim Matters Post on Halal Mortgages. MuslimMatters. https://muslimmatters.org/2012/05/08/response-to-muslim-matters-post-on-halal-mortgages/

Thank you for writing this article. You seem knowledgeable about the contract structure Guidance Residential uses. I think the Muslim community should normalize ways of financing homes outside the interest based banking system. Ways such as co-ops, seller financing, LLCs . Could you write something in the future detailing how these contracts could and should be setup (say 5 people buying a house with 20% share) to purchase and own property ?