Do credit card rewards programs have riba?

Anatomy of a transaction

Based on the Quran and Sunnah, I present the case for why credit card reward programs are halal. Please note that this does not cover cashback credit cards.

Transactions in question

I use my Chase Sapphire Preferred card to buy a $1000 American Airlines ticket, which includes a $15 credit card transaction fee.

In this example, there are four transactions.

I spend $1000 on a flight.

I pay Chase $15 for processing the payment, receiving rewards, and related services.

I repay the $1015 loan to Chase later.

I pay $85 annually for access to the payment network and benefits like no foreign transaction fees, fraud protection, and other card-specific perks (usually paid upfront).

Some important concerns

There are concerns with credit cards, and we will go through them one by one.

Asking someone else to make a payment on your behalf

Signing a contract to pay riba if you are late to payments

Getting rewards in exchange for borrowing from a credit card

If rewards are likened to currency, then considering them as a form of future currency exchange could be viewed as a form of riba

Credit cards make the majority of their money from riba, not from payment transactions.

In summary, it’s fine to pay someone to buy something for you. There is evidence that our Prophet ﷺ did not invalidate the whole contract, as long as the invalid clause was not implemented. And rewards programs are coupons, not currency.

1. Is it permissible to pay someone to buy on your behalf?

Yes. By unanimous consensus. We do this all the time already with debit cards. It is worth noting that the Quran has permitted paying the zakat collector. If we can pay people to collect zakat, then we can pay people to collect a flight ticket.

2. Can you ask someone to make a purchase for you and then pay them back later?

Yes. By unanimous consensus.

3. Is an entire contract impermissible if it includes a riba penalty for late payments?

No. This is backed by the hadith related to Barira (R). Aisha (R) wanted to free a slave. But it had an invalid clause on the contract. The Prophet ﷺ annulled the clause, but let the contract go through. This led to the slave being freed.

It is well-known that credit card contracts all include a haram riba clause for late payments. In Islam, if a contract is valid but includes one invalid condition, the contract remains valid—as long as that condition is not enforced.

But there’s more. Is intending to steal sinful if not acted on? No, and it’s a classic question in fiqh.

The same applies to riba, where the sin is in witnessing riba, paying it, or consuming it. But if no riba actually takes place, then no sin has occurred. Even if a person intends to practice riba but later does not do it, they have not committed any bad deeds. Allah knows best.

The Messenger of Allah ﷺ said, “Allah, the Mighty, and Sublime, has forgiven my Ummah for what is whispered to them or what enters their minds, so long as they do not act upon it or speak of it.”

The Prophet ﷺ said, “Allah ordered (the appointed angels over you) that the good and the bad deeds be written, and He then showed (the way) how (to write). If somebody intends to do a good deed and he does not do it, then Allah will write for him a full good deed (in his account with Him). Suppose he intends to do a good deed and did it. In that case, Allah will write for him (in his account) with Him (its reward equal) from ten to seven hundred times to many more times: and if somebody intended to do a bad deed and he does not do it, then Allah will write a full good deed (in his account) with Him, and if he intended to do it (a bad deed) and did it, then Allah will write one bad deed (in his account).”

4. Can the borrower benefit from loan?

Yes. The borrower is benefiting from the loan, not the lender. It matters because the lender can’t benefit from a loan. In Islam, the whole purpose of a loan is for the borrower to benefit.

Furthermore, the rewards points are not tied to the loan. In credit card rewards programs, they are tied to the purchase. You will get reward points regardless of whether you pay your loan or not. This shows the reward points are most commonly tied to the purchase. However, you should know that after several months of delinquency, Chase can withhold your reward points as collateral for the loan.

Rewards points are not granted immediately but after the “statement closing” date. This is not the ”payment deadline”. The “statement closing” date is the date on which your purchases are counted, and you are granted points in exchange and sent a bill. The “payment deadline” comes 25 days after the statement closing date. If you miss the “payment deadline”, you pay riba.

5. Are credit card rewards considered impermissible because they involve deferred currency exchange?

No. Credit card rewards are not currency. It’s more appropriate to think of reward points as coupons.

It matters because if it was currency, the Prophet ﷺ banned currency trades settled at a later time. Currency exchange can only be done as a spot transaction.

Reward points may resemble currency in some ways, but they aren’t the same. You can’t freely buy or sell them due to credit card rules, and doing so could get your points canceled. They're usually non-transferable—except to certain frequent flyer programs—and they can expire, unlike real currency.

Credit card reward point can be exchanged for US dollars. But only with one entity. The credit card issuer. You can exchange points for US dollars with Chase, at a disadvantaged rate. This would be self-defeating to anyone who understands the benefits of reward points. Also, currency transactions are halal, as long as they are spot transactions. Currency exchanges are haram if done with a delivery date in the future.

6. Can we do halal business with people who earn mainly from riba?

Yes. The Prophet ﷺ conducted business with Jews in Madinah. As well as many other Companions. Yet, the Jews in Madinah were known to be involved in riba. This is confirmed by statements from Abdullah bin Salam (R), a Jewish scholar who converted to Islam during the Prophet’s ﷺ time.

On a side note, credit cards have two revenue streams. Riba and access to payments network. In the payment network, they charge every transaction at the rate of 2% to 3.5%. That’s 8 times more than countries in Europe.

![U.S. Credit Card Market Share - Facts & Statistics [2022]](https://substackcdn.com/image/fetch/$s_!KX1b!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F020f3e37-6ec5-4416-b500-5ff0bfa5f3a1_732x667.png "U.S. Credit Card Market Share - Facts & Statistics [2022]")

Did I over-simplify the transaction?

Yes. To make the explanation easier to understand. This is what happens, step by step.

Related history

Bank of America created the modern credit card in 1958. Their great idea was to charge interest for late monthly payments. To get people hooked, Bank of America mailed out 60,000 credit cards to a city near Los Angeles. And the rest is history.

Card payments had no interest before 1958. The original “charge cards” had “no penalty or interest charges for payments made after 30 days”. They made money by processing transactions with a 7% fee.

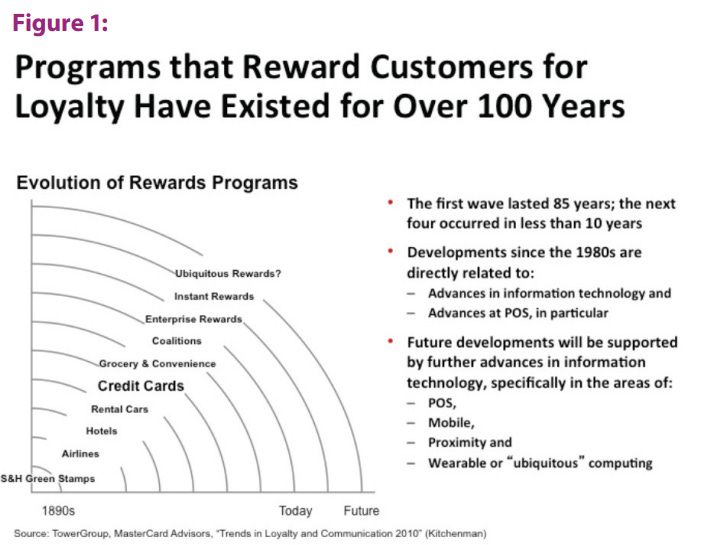

Yet, rewards programs are an old idea. In 1793, an American merchant encouraged customers to come back to his store by offering copper tokens. They would get a token for every purchase. They could use these tokens to buy something from the store.

In the 1890s, “trading stamps” became a thing. Essentially the first mass-scale rewards program. Groceries, shopping centers, gas stations. They gave stamps that could be traded in bulk from the megastore — Schuster and Company. Then, even Kellogg cereal boxes started giving out loyalty coupons.

Modern rewards programs started with airlines (1981) and credit cards followed (1991).

This is part of my series on Interest Free Zone: All of the Sahih hadith related to riba, A study of weak hadith on riba, Defining riba, A detailed breakdown on why Islamic mortgages are backdoor riba, Do credit card rewards programs have riba?, Madness on options riba

Related, I have a Riba and Ruin series: Economics is to keep you a dummy, What happened to SVB?, Ward of the State, First Republic: A tale of a fake bank & a fake auction, Hush, hush, a small bank goes poof

Related, I have a Selling Islam series: Salaried Shaykhs, Can paid Shaykhs make mistakes?

References

Abu Essa. (2019, September 16). Are Cashback Rewards On My Bank Account/Credit & Debit Cards Allowed? [Facebook video]. Almaghrib. https://www.facebook.com/almaghribworld/videos/are-cashback-rewards-on-my-bank-accountcredit-debit-cards-allowed-shaykh-abu-ees/377946566219921/

IslamQA. (2022, June 23). Ruling on discount coupons. https://islamqa.info/en/answers/121759/ruling-on-discount-coupons

IslamQA. (2005, January 6). Ruling on brokerage. https://islamqa.info/en/answers/45726/ruling-on-brokerage

Lambert, T. (2021, January 25). History of Credit Cards. Forbes Advisor. https://www.forbes.com/advisor/credit-cards/history-of-credit-cards/

Mahajjah Institute. (n.d.). Barirah. https://mahajjah.com/barirah/

Steinberg, E. (2019, August 20). Earn Points When You Don’t Pay Your Credit Card Bill. The Points Guy. https://thepointsguy.com/news/earn-points-dont-pay-credit-card-bill/

Tsosie, C. (2016, August 29). What The First Credit Cards Were Like. Forbes. https://www.forbes.com/sites/clairetsosie/2016/08/29/what-the-first-credit-cards-were-like/?sh=69b5cac75ec9

Turner, M. A. (2012, August). Alternative Data Credit Card Rewards: Context, History, and Value. Policy & Economic Research Council. https://www.perc.net/wp-content/uploads/2013/12/WP-2-Layout.pdf

Xu, C., & Reppucci, J. (2023, March 4). The Dirty Little Secret of Credit Card Rewards Programs. The New York Times. https://www.nytimes.com/2023/03/04/opinion/credit-card-rewards-points-poor-interchange-fees.html