Counting the barrels

For all the oil lost in Hormuz, where did the replacement come from

Disclaimer. Most of my portfolio is invested in oil currently.

How is it possible that Iran can shut down the Strait of Hormuz, and the oil price today is hovering around pre-war levels?

Now you think it’s clearly manipulated. But how?

The explanation is far more interesting.

To understand why oil prices haven't exploded. You need to understand the answer to this… if the world isn't getting its oil through the Strait of Hormuz, where is it getting its oil from today?

Some basics

We will measure everything in millions of barrels per day (mbd). That’s the standard of any oil earnings report. That’s what we will use.

The world consumes roughly 100 mbd. Give or take a few, depending on which season. Before the conflict, about 20 mbd passed through the Strait of Hormuz.

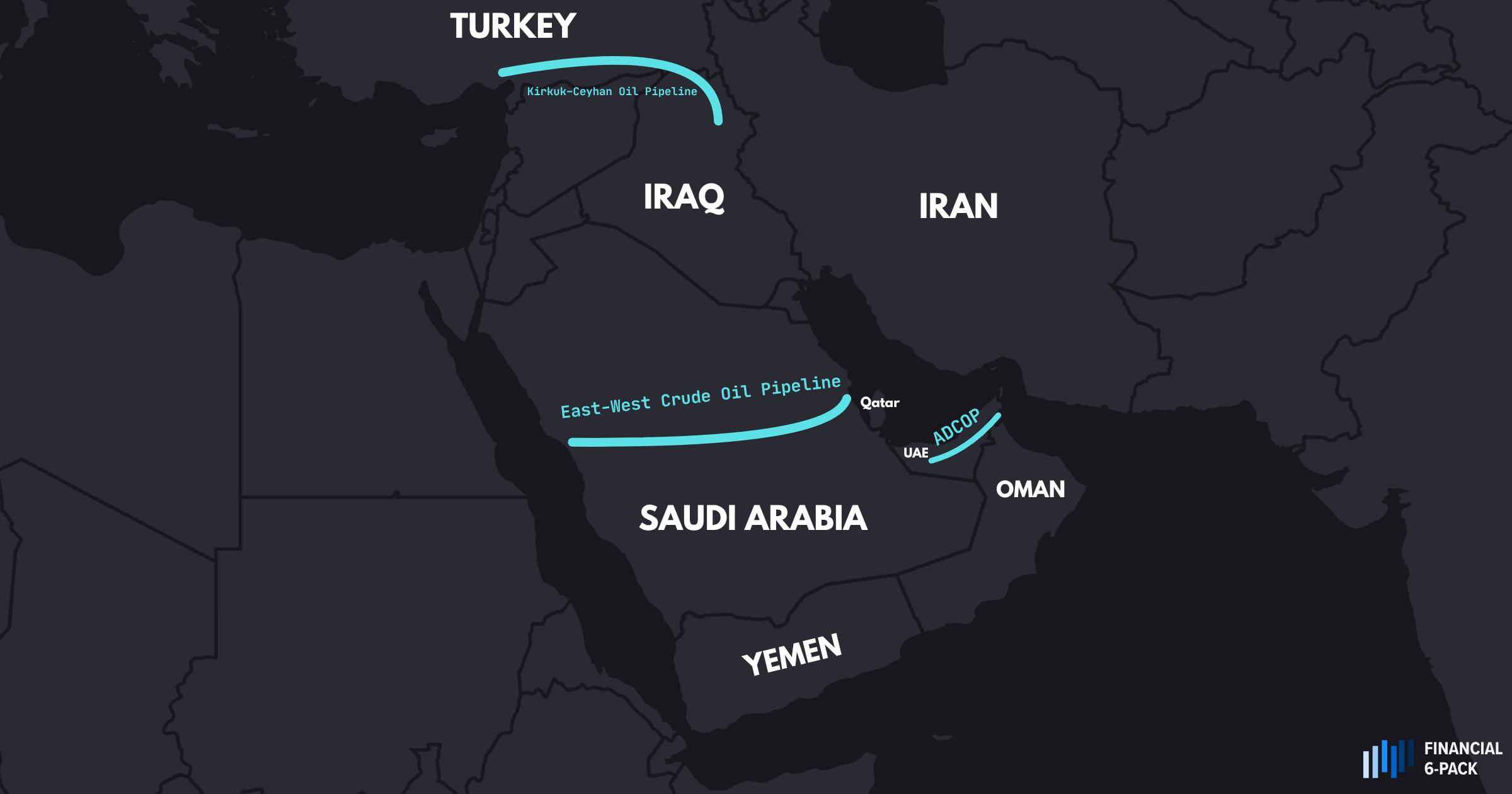

After Hormuz closed, what were the alternative routes?

The only major alternative routes were Saudi Arabia’s East–West Pipeline (7 mbd), the UAE’s Habshan–Fujairah ADCOP Pipeline (1.5 mbd). And only Iraq’s northern export route (1.6 mbd per day). Together, these routes could bypass only 10 to 11 mbd.

But this is an overly generous reading. Multiple bottlenecks constrain them.

The East–West pipeline is limited by ship-loading capacity at Yanbu, capping exports at about 4.5 mbd.

ADCOP was already running at 71% utilization before the war, leaving only ~0.4 mbd of spare capacity.

The Iraq–Turkey route is further limited by prior conflict damage tied to Kurdish areas, reducing usable capacity to roughly ~0.3 mbd.

In the real world, this crisis rerouting is only up to 6 mbd.

And remember, the Iranian oil at 2 mbd didn’t need a bypass. The West wasn’t incentivized to block them. And Iran isn’t going to stop making money.

So, that’s how 8 mbd out of the 20 mbd still flows.

Okay, so now we are at 8 mbd. Since the war, has any other country increased oil production?

Yes.

United States crude exports have jumped about 1.75 mbd.1

Venezuela is exporting 0.75 mbd more than it was before the coup against Maduro.2

Then, small amounts by Angola, Brunei, Oman, Argentina, and Gabon.3 A look at the data suggests those five countries added roughly 0.3 mbd combined.

Okay, so now we are at 11 mbd. Did any oil slip through Hormuz unofficially?

Yes. About 0.9 mbd.

That drawdown played out over roughly 3.5 months.

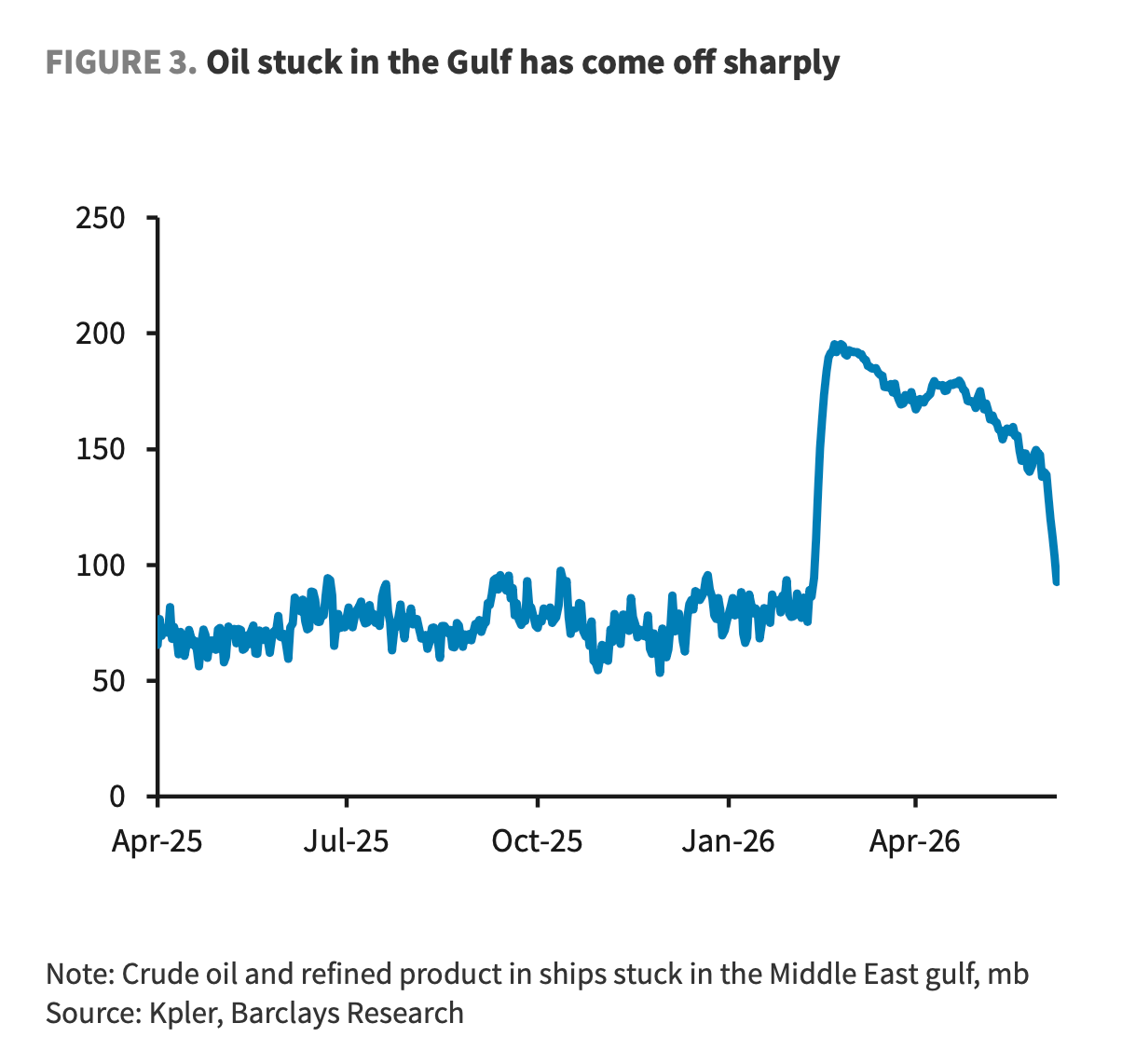

At the onset of the war, there were around 200 million barrels that was trapped in Hormuz. Just sitting there that were already pumped out of the ground into the tankers, but the tankers couldn’t move out. This is what they refer to as trapped vessel inventory.

In the last three to four months, around 100 million barrels of oil tankers were able to slip through Iran’s blockade.

Remember, no oil embargo fully works. Ask Iran, which has been sanctioned since 2018. Ask Russia, which was sanctioned in 2022. They developed workarounds. Now, the same thing happened in reverse against Iran.

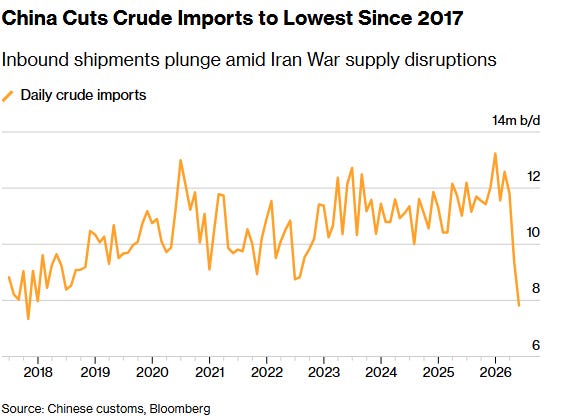

Okay, so now we are at 12 mbd. What did China do?

Most interesting, China reduced its crude oil imports by about 4 mbd.

It’s a lot. And it tells us a lot. Their demand appears to be tactical rather than structural. It tends to step back into the market when oil prices fall into the $70–80 per barrel range, taking advantage of lower prices to build its strategic petroleum reserves.

How did they cope? Less oil as a transportation fuel, while EV use has increased. More oil is going into making plastics, chemicals, fertilizers, and synthetic fibers.

Okay, so now we are at 16 mbd. What about the world's oil reserves?

The largest oil reserves in the world are with China, the USA, and Japan.

We don’t know the exact numbers of reserve depletion for China. But satellite data makes it appear they aren’t using their reserves yet, according to an oil analyst.

The United States of America has an oil reserve called the SPR. The USA began to deplete its oil reserves at 1.2 million barrels per day. And there are commercial inventories as well that are being depleted. But remember, we can’t double-count this number as it’s already reflected in US oil exports. In essence, the US is shipping its oil reserves out as exports. To primarily Europe.

Japan had to raid its strategic reserves at an unprecedented rate just to keep refineries running and industry functioning during the Hormuz closure. They depleted their oil reserves at 0.8 mbd.

The rest of the world combined has committed to releasing its stockpiles. And that averages to approximately ~1.3 mbd.

Okay, so now we are at 18 mbd. What else?

Here come the small unknowns. Outside of trapped oil inventory in Hormuz, there is floating storage of oil around the world. It’s when crude oil is kept on ships at sea instead of in land tanks. Nobody knows this data. At least I don’t.

Then you have “softening demand” for oil in some Asian countries. This suggests that countries are finding alternatives as oil becomes too costly. In reality, it means that these countries can’t get oil, and they are starting to feel pain.

Wow, so we don’t need Hormuz, since we survived?

Absolutely not. Almost half of the Hormuz replacement is being met with temporary reserves that are running out.

USA SPR and commercial inventory - over 1.5 mbd.

Japan reserves - 0.8 mbd

Other world reserves - 1.3 mbd

Trapped inventory - 0.9 mbd

Floating storage - a little

Total - around 5 mbd

And China’s demand is down by 4 mbd. That doesn’t mean it can stay that way. There was a reason they were buying oil during peacetime, whether to fill up reserves or support domestic needs. When China comes back to the market as a full buyer, it would completely overwhelm the oil demand.

So, how long before the reserves run out?

That’s the big question.

The SPR hits the tank bottom when the reserves hit somewhere between 250 mb and 300 mb. The physical storage itself has a floor below, which you can’t access without damaging the caverns.

When the oil in the reserves runs out, residents of oil exporters like the USA won’t feel the pain of demand destruction. It’s the oil importers that will feel the pain. Asian countries like Japan and India. And European countries like Germany, and so on.

I have heard many experts say that by mid-July to August, is when the artificial suppression begins to end. SPR exhaustion, trapped vessel inventory cleared, floating storage drawn down. And the deficit becomes undeniable.

Remember, 80% of world trade goes through the sea. And almost all of it is powered by oil. The world relies on oil for jet fuel, plastics, fertilizers, and asphalt. No battery can replace that.

What other problems are related to Hormuz?

The middle lane of Hormuz is still mined. These 80 mines force ships to hug the Omani coast or the Iranian coast as they leave Hormuz. The middle lane is full of mines and cannot be used until cleared. Full pre-war traffic volume is physically impossible until mine clearance is complete.

Insurance costs for the oil tankers remain a volatile deterrent. They don’t just fix overnight. Without insurance, these tankers don’t move out of Hormuz.

Iraq, Kuwait, Qatar, and Bahrain have zero bypass infrastructure around Hormuz. These countries represent 49% of Hormuz crude flows. Half the oil moving through the strait had no alternative route whatsoever. Because they can’t export, they can’t pump from their wells. This forces the wells to close. And when they are closed, they need massive injections of gas and water to open up again, which takes a few months to get them running.

A refinery that needs crude to keep running will pay whatever it takes to secure barrels because the alternative is shutting down and restarting. That costs more than any price spike. Airlines, chemical plants, and power generators face the same problem.

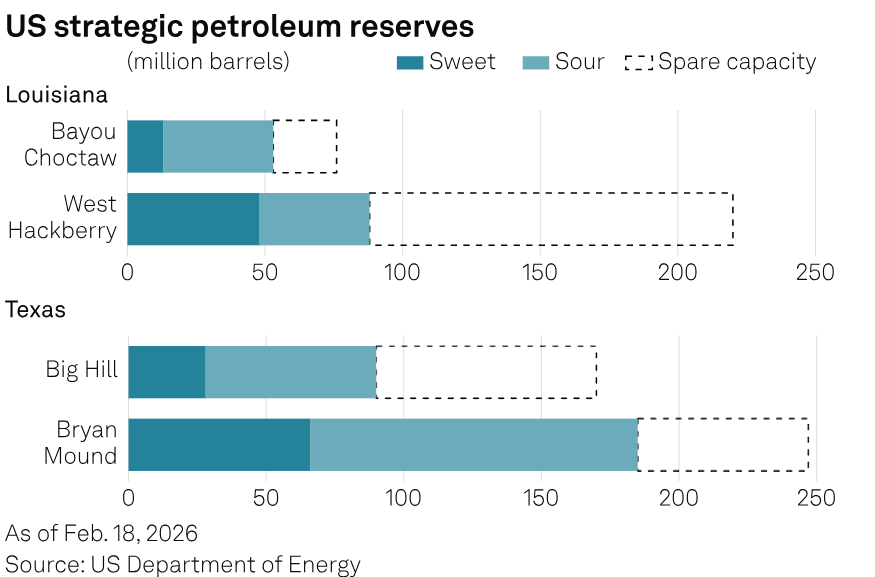

The SPR isn’t just “one bucket of oil”. It’s draining mostly sour barrels rather than sweet barrels for the refiners. This will be costly to refiners.

Almost a fifth of Qatar’s natural gas production was destroyed by the war.

If a tanker normally gets through Hormuz and reaches an Asian destination in a few weeks, a closure can turn that into a month-plus journey once waiting time, rerouting, and port congestion are added.

Hoarding. Countries like Japan will need to rebuild their inventories. At 10-15% above normal import rates takes an estimated 6-8 months, creating persistent demand.

Increased demand is incoming due to the summer months.

Risk of US-Iran war restarting. Also, the Houthis can shut down Bab al-Mandab completely. That means every Yanbu barrel bound for Asia picks up 30 days of additional voyage time and more than doubles the tonne-miles the global tanker fleet has to absorb.

At any time, tens of millions of barrels are stuck in transit. Think of it like water flowing through a very long pipe. That “water already in the system” is 80 days of oil. So 80 days is the bare minimum for the system to function. Anything below it, parts of the chain would literally run out of oil before the next shipments arrived. When it hit 79 days in mid-2008, oil went from $80 to $147.

Will Hormuz ever return to 20% of global demand? It definitely does not seem like anytime soon.

Look at the charts yourself

For Venezuela, exports were previously 0.5 million barrels per day. Today, they are around 1.25 million barrels per day.

For Brunei, exports were previously 1.81 million barrels in April 2025. There are around 2.74 million barrels in April 2026. That’s monthly data, not daily data.